An odd event took place in Hangzhou, China at the G20 Summit in September. The World Bank issued 3-year infrastructure bonds to mainland Chinese investors denominated in special drawing rights (SDR), the currency reserve basket of the International Monetary Fund (IMF), which is unique because (see Exhibit 1) it’s comprised of several national securities weighted alongside one another, including the US (42% of total), European Union (31%), Japan (8%), Great Britain (8%), and (now) China (11%). The offering of SDR bonds, which pay a blended annual interest rate of 0.5% based on the weighting of the national currencies, was unusual for several reasons. Not only was the SDR bond issue the first since 1978, but it also took place in mainland China, where citizens have historically been restricted (by tight capital controls) from holding foreign securities. What’s more, the SDR offering was launched in conjunction with the IMF’s decision to expand the SDR currency basket to include China’s currency, the renminbi (RMB), marking the first-time the currency basket has been expanded since the euro in 1999.

If you have never heard of a SDR bond, you are forgiven. Prior to the September launch in Hangzhou, there have only been two SDR bond offerings (in 1970 and 1978) since the currency unit was first-introduced by the IMF in 1968. The SDR bonds that do exist also can’t be freely-traded and are entirely held by central banks in relatively small amounts, with IMF data showing SDRs equal to just 3.24% of central bank holdings in 2014. But, recent developments suggest their use is expected to rise dramatically. That was the message from People’s Bank of China (PBoC) officials, who told media the SDR offering was 2.5x oversubscribed by buyers, who included Chinese banks, insurance companies, brokerage firms, and foreign institutions, and that, based on its success, future SDR bond issues should be expected from Chinese state-controlled development banks. IMF chief, Christine Lagarde, told reporters in Hangzhou: "The IMF was really encouraged by the determination of China to use the SDR as a yardstick to measure reserves and as a currency for bond issuance."[1] Reuters described events differently, saying: “China has been calling for a greater use of the SDR as a way to challenge the hegemony of the USD.”[2]

What is China’s end game? Three take-aways can be made. Most broadly, (1) PBoC support for the SDR bond issue in mainland China tells us that Beijing authorities have decided to promote the IMF’s SDR unit as the global reserve currency of choice over the USD. That is not a new idea. PBoC governor, Zhou Xiaochuan, first proposed measures to the IMF in 2009 that would allow the SDR to “fully satisfy the member countries’ demand for a reserve currency,” including a substitution account permitting the exchange of US Treasuries (UST) directly into SDR bonds, and the Hangzhou offering by The World Bank brings us one-step closer to that vision. From China’s perspective, the SDR is attractive because it permits an arms-length relationship with the global financial community, which would raise concerns over capital controls and rule-of-law in China, if the RMB were being promoted directly against the USD. Also, the IMF resets the country allocation of the SDR currency every 5-years, so the mechanism provides a path for the RMB to rise in share (against the USD) at a managed pace; what is known in Beijing as “crossing the river by feeling the stones.”

More immediately, we can expect (2) Chinese state-controlled development banks, including the Asian Infrastructure Investment Bank (AIIB), China Development Bank (CDB), and Silk Road Fund (SRF), to issue SDR infrastructure bonds to fund the $1.25 trillion in commitments that they, together, have made to 900 projects in 60 countries, encompassing 4.4 billion people and 40% of global economic output. That’s a big deal. After all, were Chinese development banks to issue $1 trillion in SDRs, it would allow for the creation of a liquid market, where UST could be exchanged directly into UST for the first-time. Data from the Asian Development Bank estimates infrastructure investment needs of $8.3 trillion in Asia between 2010 and 2020, so there is plenty of runway for a liquid SDR market to be developed alongside the $14 trillion market for US Treasuries (UST). Lastly, (3) the PBoC has pledged financial support to the AIIB, CDB, and SRF, so we can anticipate a portion of its foreign reserves – equal to $3.12 trillion, of which $1.12 trillion is held in UST – to be sold-down and exchanged for newly-issued SDR bonds. Why not? How would you exit a $1.12 trillion UST position? It’s a clever way for the largest holder of UST to unwind an outsized position, when there is no obvious buyer, particularly because the SDR unit has been blessed by the wider international community and a liquid market can be created with capital already held by the PBoC.

To understand the market impact of a freely-tradeable SDR, it is useful to know that the US Government (on two occasions) resisted pressures from IMF member countries to accept a substitution provision that would have enabled SDR bonds to be directly exchanged for USD assets through the IMF. John Williamson, senior fellow at the Peterson Institute, explains: “The basic proposal was that dollar holders would have the right to present their excess dollar holdings to the IMF, which would then issue an equivalent value of SDRs.” Why push-back? Because it would have “resulted in the United States accepting an SDR-denominated liability,” which means higher costs for new UST issuances. Were investors able to exchange UST for SDR bonds, one might even conclude the US would lose its ‘exorbitant privilege,’ the term coined in the 1960s by France’s Ministry of Finance, Valery Giscard d’Estaing, to explain the asymmetric advantage of the US Treasury that entitles it to pay UST holders with (only) newly-issued UST at maturity.[3] That might sound crazy, but it’s true. Economist Barry Eichengreen describes the benefits of exorbitant privilege in the US, saying: “It costs only a few cents for the Bureau of Engraving and Printing to produce a $100 bill, but other countries [have] to pony up $100 of actual goods in order to obtain one.”[4] McKinsey Global Institute estimates exorbitant privilege contributes between 0.3-0.5% to US gross domestic product each year.[5]

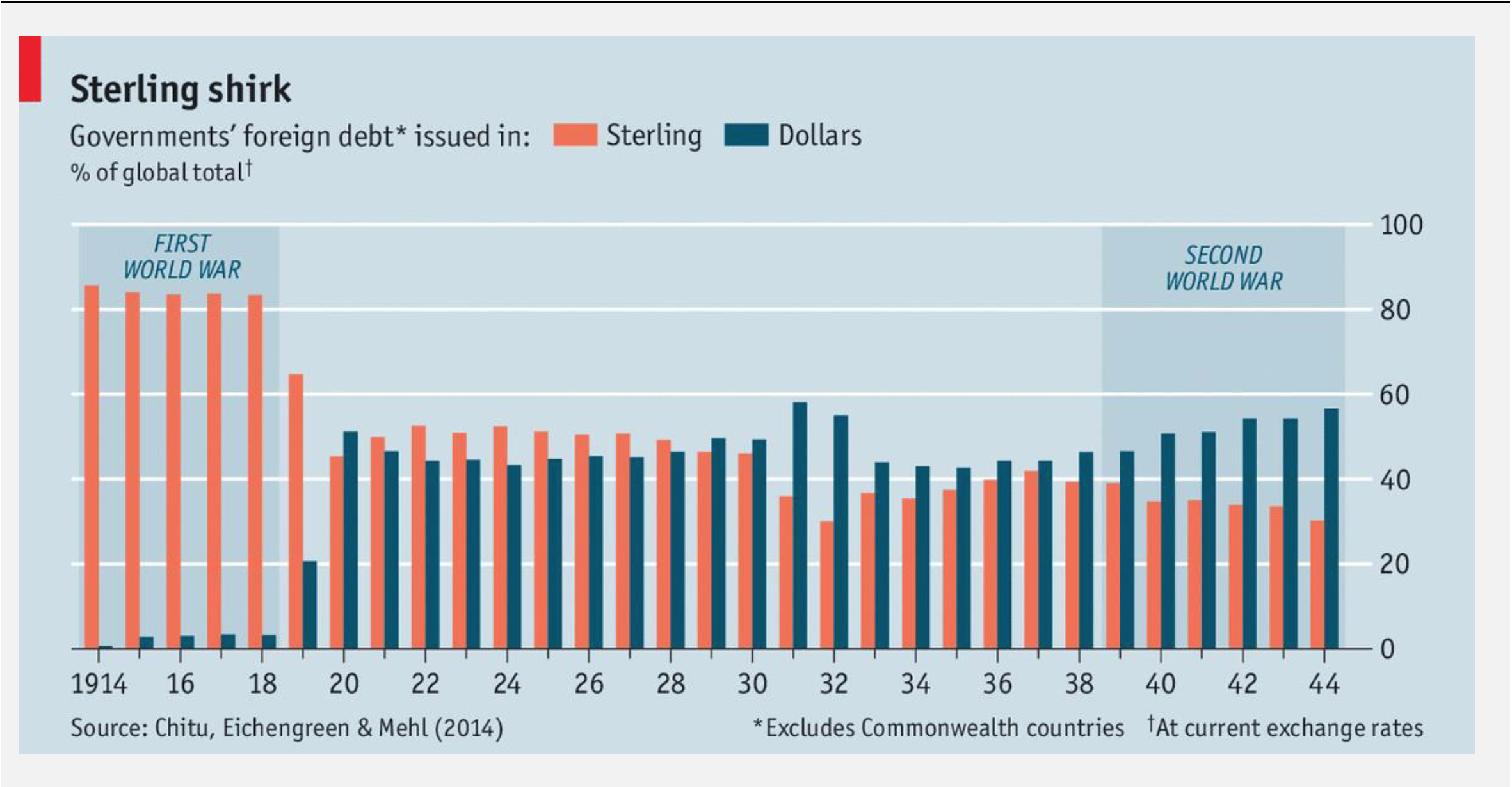

While the pace of future bond issues is impossible to predict, mechanisms are now in place that provide a clear path for new SDR bond offerings to compete directly with US Treasuries. That much is clear. No additional approvals are required from the international community. When the IMF revisits the composition of the SDR basket again in 2020, the RMB will be used far more widely, justifying a higher weighting. By comparison, US economic output will have fallen to 15% of the global total in 2020, well below the 22% figure recorded in 1990, suggesting a lower weighting. Thereafter, we can expect the SDR weighting attributed to the USD (now at 42%) to systematically lose-ground to the RMB (added at an 11% share), giving reason to a prediction from The World Bank that the USD will lose dominance by 2025 and be replaced by a multinational system that also includes the RMB and Euro.[6] Were the SDR to directly compete with UST issuances, as events suggest, it would not be the first time a long-held reserve currency were unseated by an upstart rival. The world has known 6 unofficial reserve currencies since the 15th century, where the lead position has lasted 94 years on average, with none having lasted more than 125 years ago. By comparison, the USD has been the world’s de facto reserve currency for 96-years. As a baseline, we can anticipate the rotation to unfold in a manner much like the last go-around, when (see Exhibit 2) the British Pound (GBP) was eclipsed by the USD, which was barely held outside of the US prior to World War I. The rotation from GBP to USD only accelerated, when foreign investors became comfortable with the forward currency risk. By 1950, USD assets represented more than 50% of all central bank reserves.

That’s what just happened in Hangzhou.

Exhibit 1.

Source: International Monetary Fund (September 2016).

Exhibit 2.

Source: The Economist (October 2015)

[1] Xiang, Li. “IMF Looks to Expand Special Drawing Rights.” China Daily, September 6, 2016.

[2] Zhou, Ina, and Frances Yoon. “China to Lead Way with Landmark SDR Bond Offerings.” Reuters, August 1, 2016.

[3] Williamson, John. “Understanding Special Drawing Rights.” The Peterson Institute for International Economics, No. PB09-11, June 2009.

[4] Eichengreen, Barry. Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International System.” Oxford University Press, 2011.

[5] “An Exorbitant Privilege? Implications of Reserve Currencies for Competitiveness.” The McKinsey Global Institute, December 2009.

[6] “Global Development Horizons – Multipolarity: The New Global Economy.” The World Bank, May 17, 2011.